As the tax deadline approaches, you may wish to consider whether you have incurred out-of-pocket expenses while serving as a volunteer on behalf of a charitable organization. If so, your expenses may be tax deductible provided they are properly substantiated. It is prudent to have your documentation in order well in advance of filing your tax return. Otherwise, you run the risk of disallowance by the Internal Revenue Service (IRS).

A federal charitable income tax deduction is available for unreimbursed travel expenses and other out-of-pocket expenses incurred while volunteering. In order for these expenses to be deductible, the organization must be a qualified tax-exempt charitable organization eligible to receive charitable contributions. Unfortunately, no deduction is available for the value of a volunteer's time or services.

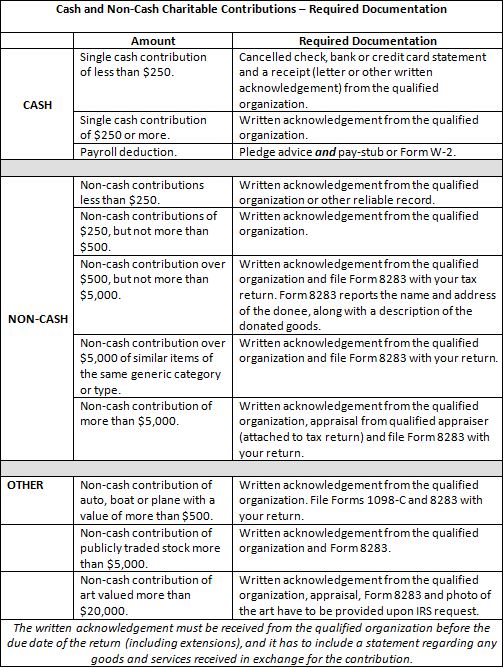

In this Alert, we summarize the nature and tax treatment of unreimbursed travel expenses and out-of pocket expenses and provide a quick reference table outlining documentation required to adequately support both cash and non-cash contributions.

Unreimbursed Travel Expenses

Unreimbursed travel expenses incurred as a volunteer on behalf of a qualified charitable organization are deductible provided there is no significant element of personal pleasure, recreation or vacation in the travel and the services performed for the charity are relevant to the organization's mission. However, the deduction will not be jeopardized simply because the volunteer enjoys the trip or enjoys volunteering for the charity.

For example, a taxpayer working on an archaeological excavation sponsored by a charitable organization for several hours each morning with the rest of the day free for recreation will not be permitted a deduction, even if he or she works hard during those few hours, as a significant element of pleasure is associated with this effort. In contrast, a charitable organization's local chapter member who attends an all-day regional meeting will not be subject to the travel disallowance rule by attending the theater in the evening.

Taxpayers can deduct travel expenses only if the work is real and substantial throughout the trip. Consequently, charitable travel costs are not deductible if only nominal duties or no duties are performed for significant parts of the trip. This personal pleasure rule also applies to expenses paid indirectly, e.g., the volunteer makes a contribution to the charitable organization and the charity then pays the travel expenses.

Deductible travel expenses include:

- Automobile mileage expenses, at the statutory standard rate of 14 cents per mile, remain unchanged for 2014. Alternatively, the costs of gas and oil directly related to the use of the auto while providing services to a charitable organization are deductible. Directly related gas and oil expenses will usually generate a greater deduction than the statutory standard mileage rate; however, receipts must be maintained. Other automobile expenses, such as repairs, depreciation and insurance, are not deductible.

- Parking fees and tolls incurred, which are deductible whether the standard rate or actual expense method is used.

- Reasonable food (subject to the 50-percent meals and entertainment limitation) and lodging costs necessarily incurred while away from home.

- Transportation costs between the airport or rail station and the hotel.

Other Unreimbursed Out-of-Pocket Expenses

Other out-of-pocket expenses incurred while rendering charitable services that are deductible as charitable contributions include specialized uniforms unsuitable for everyday use, equipment, copying charges, office supplies, long-distance charges and postage. Other examples of out-of-pocket costs and their deductibility include:

- Costs incurred by a taxpayer to entertain individuals to promote a charitable organization's program, excluding the value of food or beverages received by the taxpayer or members of his family;

- Travel expenses incurred as a volunteer to a symphony orchestra on an overseas tour, which would not be deductible when the travel includes considerable sightseeing and other personal expenses; and

- Costs incurred for caring for foster cats as a volunteer for an animal shelter or similar organization specializing in the neutering and care of wild cats (household utilities, veterinary services, pet supplies and cleaning supplies).

Substantiation Requirements

Unreimbursed volunteer expenses have the same substantiation requirements that apply to cash contributions. To substantiate a cash gift, a donor must produce one of the following:

- A cancelled check;

- A receipt; or

- When neither a cancelled check nor receipt is available, "other reliable written records" showing the donee's name.

Additionally, for expenses of $250 or more, the following are required: a letter or other acknowledgement from the charity showing the donee's name, a description of the services provided and a statement as to whether the charity provided any goods or services in return for the services and, if so, a description and a good-faith estimate of their value (or a statement that only intangible religious benefits were provided).

It is essential to obtain the required substantiation prior to the filing of your income tax return. Although many charities automatically provide written acknowledgments to their donors, they are not required to do so, except in the case of certain quid pro quo donations (where the donor received goods or services). Therefore, the donor often bears the responsibility for requesting and obtaining the necessary documentation from the charity. If you incur unreimbursed travel and other out-of-pocket expenses, it may be worthwhile to maintain the necessary documentation and consult with your tax advisor to ensure you maximize the associated tax savings.

Below is a quick reference table summarizing documentation required to support both cash and non-cash contributions.

For Further Information

If you would like more information about this topic or your own unique situation, please contact Steven M. Packer, CPA, Tracey Kuehn, CPA, or any of the practitioners in the Tax Accounting Group. For information about other pertinent tax topics, please visit our publications page located here.

Disclaimer: This Alert has been prepared and published for informational purposes only and is not offered, nor should be construed, as legal advice. For more information, please see the firm's full disclaimer.